How Bulo Helped Kashind with a Modern Risk Decisioning Platform.

See Case Study/ A BULO RESEARCH & SYSTEMS PAPER /

Behavioral Confidence for a Voice-First Economy

Decisions shouldn’t wait for paperwork. They should happen where intent is clearest, inside the conversation itself.

/ ANURAG & OM

In regulated and high-value industries, critical decisions are made in real time during verification calls, underwriting conversations, sales inquiries, and fraud reviews. Yet most risk and growth systems still treat conversations as secondary artifacts rather than primary intelligence sources.

Institutions rely on bureau files, structured applications, CRM entries, and post-call audits. The interaction becomes documentation, not infrastructure.

What remains invisible is confidence.

Confidence is reflected in narrative stability, response timing, disclosure clarity, and behavioral consistency under pressure. These are measurable variables. When structured correctly, they improve risk selection, operational efficiency, and conversion outcomes without replacing existing models.

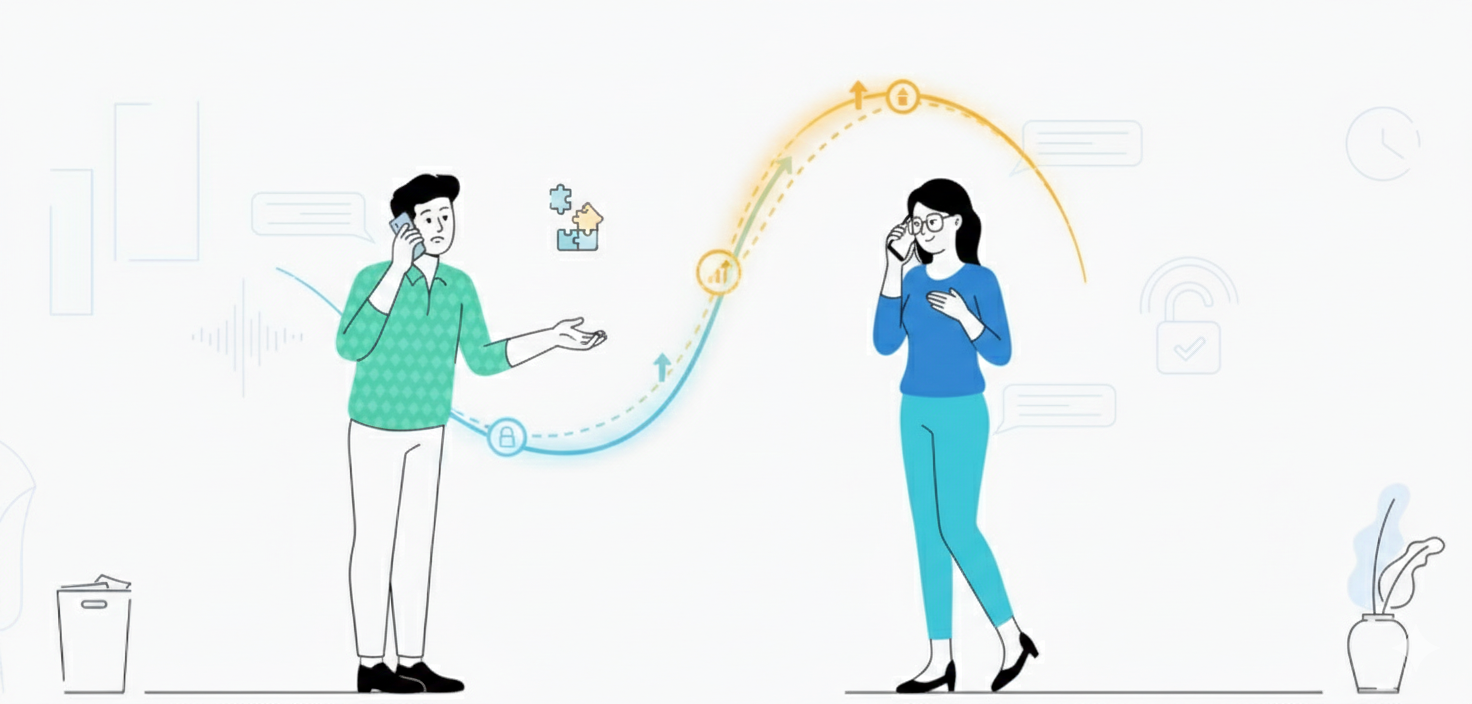

Behavioral Confidence is Bulo’s intelligence layer that converts conversational interactions across voice and assisted channels into real-time, decision-ready signals. It evaluates not only what was said, but how consistently, coherently, and confidently it was expressed.

The Voice-First Reality in India

India is not transitioning to voice. It is already voice-dominant in high-trust, high-friction decisions.

Hundreds of millions of consumers are more comfortable explaining income, negotiating price, clarifying doubts, or resolving disputes over a call rather than through long digital forms. In lending, tele-verification remains a core underwriting step. In real estate, discovery and conviction are built conversationally. In collections, repayment intent is understood through dialogue long before it appears in structured data systems.

At the same time, India is multilingual, dialect-diverse, and context-heavy. Written applications often compress nuance, while conversations expand it. The richness of voice carries behavioral signals that structured forms cannot capture, including shifts in certainty, coached responses, hesitation under financial disclosure, or clarity when discussing repayment commitment.

Yet most institutions still treat voice as a compliance artifact rather than a decision surface.

This creates a structural mismatch. Decisions depend on conversations, but decision systems depend on static data.

Behavioral Confidence exists to close that gap, particularly in markets like India where voice is not an auxiliary channel but the primary trust interface between institutions and customers.

The Three Pillars of Behavioral Confidence

Behavior is the missing variable in modern decision systems.

Pillar I: Structured Behavioral Signals

Every interaction processed through the Behavioral Confidence Engine™ is transformed into structured variables that quantify narrative consistency, hesitation patterns, disclosure resistance, cognitive load shifts, and engagement strength.

Signals are language-agnostic and calibrated for multilingual environments. The system measures timing, density, and response stability rather than relying solely on keywords or sentiment classification.

In live environments, signal extraction occurs within sub-second latency, with variance detection typically under one second from response completion. Repeat-question consistency tracking demonstrates stable pattern detection across structured verification flows without requiring rigid scripts.

This pillar ensures that conversations are converted into measurable behavioral datasets rather than stored as passive recordings.

Pillar II: Contextual Decision Mapping

Behavioral signals must be interpreted within workflow context. A pause during income disclosure carries a different implication in underwriting than in a sales discovery call.

The engine maps signals across the full decision lifecycle:

- Lead qualification and intent scoring

- Onboarding and KYC verification

- Credit underwriting and thin-file assessment

- Fraud detection and anomaly review

- Disbursement confirmation and compliance checks

- Collections prioritization and recovery monitoring

- Portfolio stress conversations and restructuring discussions

This lifecycle mapping allows behavioral confidence to persist beyond acquisition and become part of monitoring, governance, and portfolio oversight.

Pillar III: Confidence Gates and Explainability

Instead of binary rule execution, the system applies calibrated confidence thresholds that regulate automation authority. High-confidence interactions can proceed with minimal friction. Medium-confidence interactions trigger structured clarification. Lower-confidence interactions escalate for review.

Each decision is traceable to specific behavioral variables. Risk and compliance teams can audit why a gate shifted, which signals contributed, and how confidence evolved during the interaction.

Confidence is measurable, defensible, and aligned with regulated decision environments.

Capturing the Full Risk and Growth Lifecycle

Intelligence should not stop at approval. It should follow the customer journey.

Most decision systems optimize for a single checkpoint, approval. Behavioral confidence extends across the lifecycle.

At acquisition, it filters high-intent prospects from speculative noise. During onboarding, it reduces unnecessary manual verification by triaging based on stability signals. In underwriting, it supplements bureau data with behavioral consistency indicators. During fraud checks, it surfaces conversational strain before documentation inconsistencies appear. Post-disbursement, it detects early narrative stress during repayment discussions, often preceding observable delinquency signals.

Across structured pilots and controlled rollouts, institutions have observed directional improvements such as:

- 18–35% reduction in manual verification workloads

- 12–25% faster decision turnaround times

- 10–18% improvement in qualified lead conversion in assisted sales flows

- Measurable uplift in thin-file approval confidence when behavioral signals supplement bureau-only assessment

- Earlier identification of elevated repayment risk signals during monitoring calls

These outcomes vary by portfolio and implementation design. Behavioral confidence is designed to augment, not replace, existing credit and fraud models.

Embedded Case Snapshot

A mid-sized digital lender operating in a thin-file segment integrated Behavioral Confidence signals into its tele-verification workflow. Instead of applying uniform manual review across all applicants, the institution introduced confidence-based triage during income and employment verification calls.

Within the first quarter of controlled deployment, the lender reduced full manual review dependency by approximately one-fifth while maintaining portfolio performance stability. Approval confidence improved in borderline cases where bureau depth was limited, without increasing early delinquency indicators.

The system did not replace underwriting models. It introduced an additional behavioral layer that refined escalation decisions.

Beyond Voice: A Unified Conversational Risk Layer

Voice remains a dominant channel in relationship-driven and emerging markets, but Behavioral Confidence is not limited to telephony. The same signal architecture can extend to assisted chat, video verification, and hybrid agent workflows.

Behavioral variables can be unified alongside bureau data, transactional signals, device intelligence, and alternative datasets within broader risk platforms.

Behavioral Confidence does not attempt to replicate full-stack risk orchestration. It strengthens enterprise risk infrastructure by introducing a structured conversational intelligence layer that traditional systems do not capture.

Technical Benchmarks and Governance

The Behavioral Confidence Engine™ operates through a real-time speech-to-structured pipeline with average signal generation between 600 and 900 milliseconds from response completion.

The architecture supports:

- API-first integration with decision engines and CRM systems

- Private cloud or controlled deployment environments

- Variable-level explainability for audit and compliance review

- Portfolio-specific recalibration

- Structured logging aligned with regulated workflows

False-positive management is governed through multi-signal aggregation rather than single-trigger rules, reducing noise and preventing over-escalation.

The system is designed to operate alongside existing credit policies and regulatory frameworks rather than override them.

Why This Matters Now

Fraud is increasingly coached. Thin-file applicants remain underserved. Manual review costs continue to rise. Customers expect faster decisions. Regulators expect stronger oversight and explainability.

Automation without behavioral intelligence introduces blind spots. Recording conversations is passive. Structuring behavioral confidence makes them operational.

The next evolution of enterprise decision systems is not broader automation. It is lifecycle-aware behavioral intelligence embedded directly into risk and growth infrastructure.

Institutions that integrate behavioral confidence across acquisition, underwriting, fraud monitoring, and portfolio management can improve prioritization, reduce operational friction, and strengthen governance without increasing model opacity.

Behavioral confidence should not sit beside the decision engine. It should inform it.

Bulo.ai

Behavioral Intelligence for Conversational Decision Systems

/ Bulo turns voice heard into trust earned.

Book a demo